Amazing! Thanks!

"Let us not seek to fix the blame for the past. Let

us accept our own responsibility for the future."

–John F. Kennedy

GOP Failed to Repeal Obamacare in July

A major effort by Republicans to “repeal and replace” the Patient Protection and Affordable Care Act [1]—also known as the ACA or Obamacare—dramatically failed in the Senate at the end of July [2] just before Congress adjourned for summer recess.

During and after that political battle, the majority of the general public continued to have increasingly favorable views of the ACA at 52%, an all-time high since Obamacare was first enacted in 2010 [3].

Contrary to sensationalized claims amid continuous political wrangling, Obamacare is neither thriving nor imploding [4]. The mix of successes and drawbacks vary by region, where some serious flaws do need to be addressed.

However, on the whole, Obamacare has helped advance the American health care system compared to pre-ACA days [5,6], but there remains much room for improvement.

Trump Continues to Undermine Obamacare

Surprisingly, the ACA has been resilient to repeated attacks over the years by the Republican establishment [7] and now also Trump [8,9], who has frequently announced his desire to “let Obamacare fail”. Unfortunately, Trump could still do much more to undermine and damage the ACA if he wanted to abruptly cripple it [10]. Regardless, many legislative fixes and improvements are still needed.

Health care organizations, hospital associations, insurers, and state governors have commented on several areas where Trump could have a substantial and immediate impact on reaffirming (or eroding) confidence in the individual Marketplace, which is the central federal exchange of contracted private insurers where consumers may purchase non-group, non-employer-sponsored health insurance.

Two of those important areas of focus to stabilize the Marketplace in the near-term are paying insurer subsidies and enforcing the law on mandatory enrollment.

Trump is Cagey and Noncommittal Toward Paying Insurers

Trump has been unclear since inauguration whether he would continue to pay cost-sharing reductions (CSR), which are subsidies paid directly to insurers by the federal government to help lower the cost of deductibles and the share of services billed to low-income earners [11].

Notably, Trump has repeatedly claimed CSRs are a “bailout”, which is incorrect and highly misleading [12]. As a condition of Marketplace participation, the ACA requires insurers to provide higher-value plans—whether or not the government upholds its promise to defray the extra costs. This uncertainty makes insurers nervous because they are now exposed to greater financial risk.

Although this Administration has reluctantly paid CSRs on a month-to-month basis (while simultaneously and routinely threatening to stop doing so [13]), Trump has not yet committed to making the payments long-term. When asked last week how the Administration intends to proceed, a Trump official vaguely suggested they “will do the minimum necessary to comply with the law” [14].

As such, for insurers who have stayed in or recently joined the Marketplace, many have included an additional 13-20% increase in the cost of premiums for 2018 under the assumption Trump will not reimburse them [15,16].

Providing a higher standard of benefits, services, and coverage mandated by the ACA without adequate compensation would be a disincentive for insurers to participate in the Marketplace. Higher costs to consumers would also be a deterrent to signing up for health insurance.

The “Individual Mandate” is a Keystone of Obamacare

The Trump Administration has also been vague on whether they intend to enforce the individual mandate [14], which requires individuals to purchase health insurance or pay a penalty.

While the individual mandate is unpopular with some Democrats and many Republicans, informed health policy advocates have urged Trump to not scrap it before coming up with a more palatable bipartisan alternative [17]. Without the mandate, the proportion of healthy enrollees and the associated funds for the entire risk pool would shrink, thereby causing Marketplace prices to balloon out of control.

(To fund the risk pool in the Republican AHCA House bill, individuals who had a gap in coverage were penalized with a rate-hike in premiums upon their return to the Marketplace, while the Senate BCRA bill required a wait period between signing up and accessing health benefits for the first time. All of these mechanisms are designed to maintain funding reserves by preventing people from only signing up for insurance immediately after becoming ill. Everyone offsets financial risk to insurers by “paying into the system” via monthly premiums, for example.)

“Listen All of Y’all It’s a Sabotage”

“Listen All of Y’all It’s a Sabotage”

(Orange Crushes ACA Outreach Efforts)

On August 31, just two months before the Marketplace begins enrollment, Trump has decided to cut spending on Obamacare advertising by 90%, from $100 million down to $10 million [18]. For comparison, California itself plans to spend $112 million on health law advertising.

Trump will be changing the type of ads and reminders too—switching from widespread TV and radio campaigns under Obama to simply emails and text messaging.

As with ads, Trump said he also plans to cut 41% of funds for the in-person community outreach and ACA sign-up “navigator” programs.

Currently, the assistance programs don’t have any funding; they ran out of grant money on September 1 [19]. Some local staff are being laid off at a time when they would otherwise be ramping up to prepare for the upcoming enrollment period. It’s unclear if Trump will continue to neglect this issue until September 30, the end of the fiscal year, although it’s not uncommon for grant letters to be sent out late.

Administration officials cited inefficient use of resources to justify their decision and noted 5% fewer people than expected signed up for Obamacare in January despite having spent more money. They failed to mention Trump pulled ACA advertising then, too—ads that were already paid for [20].

Advertisement and outreach funding are important because the highest rate of sign-ups occur right before the enrollment deadline [21].

Although sicker individuals are generally more vigilant about not missing the sign-up window—which Trump has shortened from 90 days to just 45 days this year (November 1 to December 15, 2017)—an estimated 40% of uninsured Americans are unaware of the Marketplace and its open enrollment dates [18].

Essentially, the fewer healthy people who sign up, the more Marketplace premiums will increase for everybody.

Some Insurers Retreat From the Marketplace While Others Enter and Expand

The deadline for insurers to file rates for their 2018 health plans was September 5, with any clarifications to be submitted by September 20 [22]. Insurers must decide whether to stay in the 2018 Marketplace by September 27 when their final signed agreements are due.

Despite significant turnover of insurer participation in the Marketplace [23]—in large part due to uncertainty of financial risks introduced by Trump [24]—by late August, no counties were left with zero insurers after Washington, Nevada, Missouri, Wisconsin, Indiana, Ohio, and Tennessee recruited at least one insurer to fill the remaining empty service regions for 2018 [25].

However, this preliminary information on insurer coverage by county is subject to change and is updated on a weekly basis [26,27].

Whether or not all counties are covered in 2018, there is still a large potential problem: almost 1,500 (47%) counties in the U.S. involving 2.7 million (29%) Marketplace participants are at risk of falling through the cracks due to having only one carrier at the moment.

(Case in point: While writing this post, Optima Health decided to scale back its participation in Virginia’s state markets leaving 63 of 95 counties that serve over 70,000 people now at risk of having no insurer for 2018.)

Maintaining Perspective on Obamacare

It’s important to note most of the health insurance landscape in America is stable [28].

Costs to families who purchase health insurance through their employer (156 million people) and costs incurred per enrollee in Medicare (55 million people), Medicaid, and Children’s Health Insurance Program (74 million people) increased by 1-4% over last year.

The non-group insurance market, which includes the ACA Marketplace and individuals who purchase health plans directly from insurers, covers 17.5 million Americans.

Of that subset of people, 10.3 million (~60% of the non-group market) get their insurance through Obamacare [29].

Of the people on Obamacare, 8.7 million (~84%) receive federal subsidies to lower the cost of their premiums. The amount of subsidies provided is tied to the cost of mid-tier plans on the Marketplace. As the cost of premiums grow, government subsidies do too—which is why if Trump doesn’t pay CSRs to insurers, his sabotage efforts could cost the government approximately $200 billion more over the next 10 years [30].

Unfortunately, the people who would suffer the brunt of premium spikes next year are the 6.7 million individuals who purchase their insurance outside the Marketplace Exchange (5.1 million people) or who don’t qualify for subsidies through Obamacare (1.6 million people) because their incomes are just above the cutoff to receive financial assistance—i.e., the middle class.

This group that is most at risk of large premium increases comprises only 3% of all insured Americans [31], but that’s still a lot of people.

Still, had Obamacare never existed, the likely cost of premiums for comparable mid-tier plans would have been 30-50% higher on average than they are now [32].

REFERENCES

1. Kaiser Family Foundation Health Reform (April 25, 2013). Summary of the Affordable Care Act. Retrieved from KFF.org on September 6, 2017.

2. Parlapiano, A., Andrews, W., Lee, J., and Shorey, R. (Updated July 28, 2017). How Each Senator Voted on Obamacare Repeal Proposals. Retrieved from NYTimes.com on September 6, 2017.

3. Hamel, L., Wu, B., Muñana, C., and Brodie, M. (August 24, 2017). Data Note: Strongly Held Views on the ACA. Retrieved from KFF.org on September 6, 2017.

4. Cox, C. and Levitt, L. (August 4, 2017). What’s the Near-Term Outlook for the Affordable Care Act? Retrieved from KFF.org on September 6, 2017.

5. Hiltzik, M. (January 4, 2017). Republicans call Obamacare a ‘failure.’ These 7 charts show they couldn’t be more wrong. Retrieved from LATimes.com on September 6, 2017.

6. Kamal, R. and Cox, C. (May 19, 2017). U.S. health system is performing better, though still lagging behind other countries. Retrieved from Kaiser Family Foundation HealthSystemTracker.org on September 6, 2017.

7. Norris, L. (May 17, 2017). 10 ways the GOP sabotaged Obamacare. Retrieved from HealthInsurance.org on September 6, 2017.

8. Center on Budget and Policy Priorities (Updated August 31, 2017). Sabotage Watch: Tracking Efforts to Undermine the ACA. Retrieved from CBPP.org on September 6, 2017.

9. Families USA Foundation (Updated September 2017). Affordable Care Act Attack Tracker. Retrieved from FamiliesUSA.org on September 6, 2017.

10. Cunningham, P. (August 30, 2017). The Health 202: Trump says Obamacare will implode. But his administration isn’t necessarily hurting it. Retrieved from WashingtonPost.com on September 6, 2017.

11. Committee for a Responsible Federal Budget. (2017, August 29). The ACA’s Cost-Sharing Reductions (CSRs): A Primer. Retrieved from CRFB.org on September 6, 2017.

12. Robertson, L. (August 2, 2017). Subsidies, Not Bailouts. Retrieved from FactCheck.org on September 7, 2017.

13. Pear, R. and Kaplan, T. (August 15, 2017). Trump Threat to Obamacare Would Send Premiums and Deficits Higher. Retrieved from NYTimes.com on September 6, 2017.

14. Pear, R. (August 30, 2017). Trump Administration Wants to Stabilize Health Markets but Won’t Say How. Retrieved from NYTimes.com on September 6, 2017.

15. Coombs, B. (August 10, 2017). Uncertainty over Trump’s health-care policies driving double-digit insurance price hikes. Retrieved from CNBC.com on September 6, 2017.

16. Sanger-Katz, M. (August 10, 2017). Obamacare Premiums Are Set to Rise. Thank Policy Uncertainty. Retrieved from NYTimes.com on September 6, 2017.

17. Smyth, J. and Anderson, J. (August 31, 2017). Governors urge keeping US health law’s individual mandate. Retrieved from ABCnews.com on September 6, 2017.

18. Kliff, S. (September 5, 2017). This is what Obamacare sabotage looks like. Retrieved from Vox.com on September 9, 2017.

19. Kliff, S. (September 8, 2017). This is the most brazen act of Obamacare sabotage yet. Trump has quietly stopped funding Obamacare’s outreach budget. Retrieved from Vox.com on September 9, 2017.

20. Demko, P. (January 26, 2017). Trump White House abruptly halts Obamacare ads. Retrieved from Politico.com on September 9, 2017.

21. Pollitz, K., Tolbert, J., and Semanskee, A. (June 8, 2016). 2016 Survey of Health Insurance Marketplace Assister Programs and Brokers. Section 2: In-Person Assistance During Open enrollment. Retrieved from KFF.org on September 9, 2017.

22. Hellmann, J. (August 11, 2017). ObamaCare deadline for insurers delayed by three weeks. Retrieved from TheHill.com on September 7, 2017.

23. Norris, L. (August 25, 2017). ‘Bare counties’ just got covered. Here’s why. Retrieved from HealthInsurance.org on September 7, 2017.

24. Alonso-Zaldivar, R. (August 10, 2017). Study says Trump moves trigger health premium jumps for 2018. Retrieved from APnews.com on September 7, 2017.

25. Bump, P. (August 24, 2017). An anti-Obamacare argument evaporates: No counties now lack exchange insurers. Retrieved from WashingtonPost.com on September 7, 2017.

26. Kaiser Family Foundation Health Reform (August 18, updated September 6, 2017). Counties at Risk of Having No Insurer on the Marketplace (Exchange) in 2018. Retrieved from KFF.org on September 7, 2017.

27. Centers for Medicare & Medicaid Services, Center for Consumer Information & Oversight (Updated September 6, 2017). 2018 Projected Health Insurance Exchange Coverage Maps. Retrieved from CMS.gov on September 7, 2017.

28. Altman, D. (August 31, 2017). How to keep ACA stabilization narrow. Retrieved from Axios.com (via KFF.org) on September 9, 2017.

29. Altman, D. (August 10, 2017). The ACA stability “crisis” in perspective. Retrieved from Axios.com (via KFF.org) on September 9, 2017.

30. Kliff, S. (August 15, 2017). CBO says Trump’s Obamacare sabotage would cost $194 billion, drive up premiums 20%. Retrieved from Vox.com on September 10, 2017.

31. Griggs, T., Yourish, K., and Sanger-Katz, M. (March 9, 2017). How Many People Are Affected by Obamacare Premium Increases? (Hint, It’s Fewer Than You Think). Retrieved from NYTimes.com on September 9, 2017.

32. Adler, L. and Ginsburg, P. (July 21, 2016). Obamacare Premiums Are Lower Than You Think. Retrieved from HealthAffairs.org on September 9, 2017.

4 Likes

@John You put so much work into these… would you be open to managing your own thread with this info? You could have different issues highlighted in the OP, and then links to posts you make in the thread detailing the most recent status of those issues.

It just seems a shame to have all this info buried in this thread where no one can really notice or appreciate it. If you decide you’re willing to do that, please put it in General Discussion for now.

2 Likes

Agreed - they are excellent! I can’t even imagine how long it must take to research plus write it up too!

2 Likes

@John yes I concur with the other messages. These posts are so detailed the deserve threads of their own. Keep up that fantastic work!

2 Likes

(This post will also be linked to in the Health Care News and Updates thread.)

Congress Returns From Recess: September 5, 2017

After Congress failed to pass a health care reform bill prior to August recess [1], Republican momentum to repeal Obamacare stalled—if not almost entirely sunk.

On the night of July 28, Senate Majority Leader Mitch McConnell (R-KY) lamented, “it is time to move on,” from trying to repeal and replace Obamacare [2].

Beyond the appearance of Republicans conceding defeat, breaking a seven year promise to their constituents, and blaming their shortcomings on Democrats, a policy pivot also reflects Trump’s impatience and frustration with a constrained legislative process. Now he wants to use this time to focus on “Tax Reform/Tax Cut legislation” instead [3]. Moreover, Congress has a backlog and a myriad of other more emergent issues to address [4].

Most members of Congress acknowledge the next step of health reform is to shore up and stabilize the ACA Marketplace to avoid jeopardizing millions of people’s health insurance. Nonetheless, there is still one GOP bill remaining—described as a “Hail Mary” long-shot—to potentially scrap Obamacare.

GOP’s use of the budget reconciliation process to reform health care expires soon—September 30, the end of the fiscal year [5].

Graham-Cassidy Bill to Repeal the ACA

Seemingly Impossible to Pass, But Not Dead Either

It’s incredibly unlikely this last-ditch effort to repeal Obamacare will meet the deadline in the next two weeks: the bill has yet to be completed (let alone debated or weighed in full), doesn’t have a CBO score, and doesn’t have support from enough Republicans to move forward [6], although some are still open to the idea.

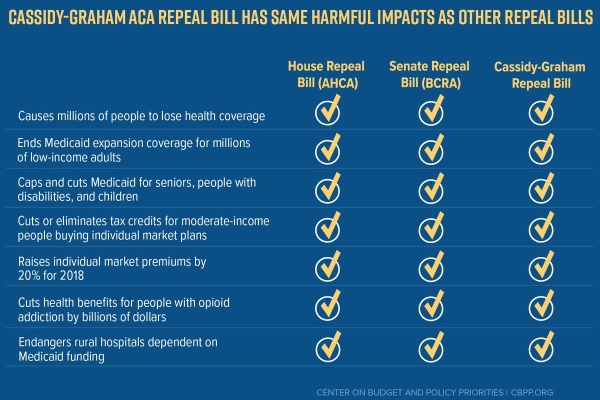

The latest draft bill proposed by Senators Lindsey Graham (R-SC) and Bill Cassidy (R-LA) emerged from the series of Republican bills rejected in July and would be the most devastating to Obamacare yet [7].

But as one insider health care lobbyist put it, “McConnell has zero interest in presiding over another goat rodeo.” [8]

Enthusiasm from Senate leadership has clearly dwindled, but Trump has nonetheless agreed to sign whatever Obamacare repeal is sent his way.

The Most Radical Attempt to Disrupt Obamacare Yet

There are several versions of text in circulation, but the most detailed one so far exists as a modified amendment to the Senate’s previous attempt to repeal the ACA [9] and replace it with the Better Care Reconciliation Act (BCRA) of 2017.

Edit: More details and analysis of the Graham-Cassidy plan as of September 13.

(click to expand) Graham-Cassidy ACA Repeal Bill Feature Summary

Cassidy marketed the bill as a way to “give power back to patients” and give states more control over spending federal dollars, which is the same refrain often used by GOP to decrease regulation, lower consumer protections, and weaken accountability of insurers [10].

More specifically, the GC bill would eliminate the individual mandate (likely causing an Obamacare “death spiral”); un-insure 32 million people; eliminate federal subsidies to private insurers (the cost-sharing reductions Trump has not yet committed to pay in the long-term); provide the least generous tax credits (making premiums less affordable); end Medicaid expansion by splitting the federal funds currently given to 30 participating states and spreading them among all 50; equalize payments to states regardless of population density (i.e., effectively redistributing federal dollars to advantage rural areas); convert some state payments to a lump-sum (a capped amount via block grants that expire after 2026); and increase flexibility of federal grants to be used as a “slush fund”—possibly diverting money once designated for health insurance to other state programs. States that are unable to match funds and pay up would not be eligible to receive federal assistance either.

See also: Trump Continues to Undermine Obamacare

While some of the cuts to financial assistance under Obamacare would potentially be provided in other ways by using the “slush fund”, there would be no requirement to focus on helping low-income individuals.

Ultimately, providing less money to states while expecting them to expand coverage simply doesn’t add up.

Stabilizing and Fixing the ACA

After returning from August recess, Senators Lamar Alexander (R-TN) and Patty Murray (D-WA) held bipartisan hearings to evaluate how to further stabilize Obamacare in the short-term [11,12].

Democrats, insurers, and providers are in general agreement with Alexander and Murray’s narrower market-stabilization approach. Some Republicans are also on board but may push for more insurance deregulation measures.

Governors Provide Congress with Solutions to Fix the ACA

A bipartisan group of governors from 7 states led by John Kasich (R-OH) and John Hickenlooper (D-CO) created a “blueprint” with specific recommendations on how to strengthen the insurance market [13,14].

Broadly speaking, the Kasich-Hickenlooper plan focuses on three main requests:

Previously, we have written that changes to our health insurance system should be based on a set of guiding principles that include improving affordability and restoring stability to insurance markets. Reforms should not shift costs to states or fail to provide the necessary resources to ensure that the working poor or those suffering from mental illness, chronic illness or addiction can get the care they need.

Based on these guiding principles, we recommend (1) immediate federal action to stabilize markets, (2) responsible reforms that preserve recent coverage gains and control costs, and (3) an active federal/state partnership that is based on innovation and a shared commitment to improve overall health system performance.

These goals could be achieved by:

- Paying insurers cost-sharing reductions.

- Creating a temporary stability fund to lower premiums and prevent excessive losses to insurers for providing greater coverage.

- Creating incentives for insurers to enter and compete in underserved counties.

- Maximizing market participation by keeping the individual mandate (for now) and continuing to fund advertisements and outreach efforts to encourage enrollment.

- Fully committing to and funding risk sharing programs designed to spread financial risk equitably across all insurers.

- Redesigning essential health benefits requirements with more state flexibility.

- Improving regulatory reforms and avoiding duplication of effort at the federal and state levels.

- Supporting state innovation waivers to tailor the ACA to meet local needs.

- Controlling costs through advancing the value-based payment system, increasing cost transparency and quality metrics of health providers to empower consumers, and more.

- Promoting bipartisan cooperation in Congress to make meaningful, lasting reforms.

Progressives Advance Their Own Set of Ideas

Medicare-For-All

As of early afternoon on September 12, eleven of 48 Democrats have signed on to co-sponsor Senator Bernie Sanders’ (I-VT) health care bill [15,16], a (presumably) more cost-effective and sustainable way to insure all Americans.

Even the most conservative Democrat—Senator Joe Manchin (D-WV), two-thirds of whose state voted for Trump—is open to learning about and exploring similar long-term options, although he remains “skeptical single-payer is the right solution” [17].

The full details of Senator Sander’s plan is set to be revealed later today (September 13, 2017) and now has 15 Democrats on board [18]. It also appears Bernie’s plan for universal health coverage is close to single-payer but might retain smaller private insurers to fill in some gaps for elective procedures like some surgeries, for example.

Apparently, Medicare-like coverage would be immediately expanded to people under 18 year’s old with everyone else phased into the program over four years. The public system would be paid for with higher taxes, but people would no longer have to pay co-insurance and businesses would no longer have to subsidize employer-based insurance plans.

Keep in mind the chances of this bill moving forward and passing in the current polarized political environment are very slim, if not impossible at this time. Regardless, the near-term purpose is to move the discussion further toward the political left, possibly opening the doors for 2020 or beyond.

Other Ways to Attain Universal Health Care

Because designing a health care system is so complex (who knew?), there may be other more politically palatable and effective incremental strategies to achieve universal coverage [19], of which single-payer is just one pathway to reach that goal.

Some suggestions include:

- Expand Medicaid in 19 more states.

- Expand state-based insurance coverage to undocumented immigrants, where favorable.

- Fix a known issue with Obamacare in which low-to-mid income families cannot afford employer insurance plans but remain ineligible for federal subsidies.

- Secure funding for the popular CHIP program for low-income children (funding expires this month).

- Continue the transition of Medicare providers’ “fee-for-service” payment models to value-based payments.

- Reduce prescription drug costs by allowing Medicare to negotiate lower drug prices.

- Regulate anti-competitive insurance monopolies.

- Promote a “public option” for people in underserved areas lacking private insurers to purchase government-sponsored insurance.

Another approach that builds upon Senator Sanders’ and Senator Schatz’s (D-HI) previous ideas has been floated by Senator Chris Murphy (D-CT) [20].

Instead of quickly transitioning to a nearly-exclusive full-benefits Medicare-based system funded up front by more taxes, Murphy’s plan would allow buy-in as a public option requiring shared payments to supplement private insurance, theoretically advancing to single-payer at a slower pace.

Too Much, Too Fast? Lessons From Trumpcare’s Failure

There are some valid concerns about abruptly pushing for sweeping changes required to establish a single-payer system—when combined with over-promising better coverage and provider access at lower cost despite backlash from special interests and a massive “sticker shock” tax hike—could cause Democrats to fumble [21].

An incremental, pragmatic, bipartisan approach evaluating specific policy details while remaining honest about difficult trade-offs and sociopolitical challenges would likely fare a better chance at passing, albeit with necessary compromises [22].

REFERENCES

1. Yadidi, N. (August 4, 2017). August recess: What is it – and what’s next? Retrieved from CNN.com on September 12, 2017.

2. Roubein, R. (July 28, 2017). McConnell: ‘Time to move on’ after healthcare defeat. Retrieved from TheHill.com on September 12, 2017.

3. Sargent, G. (September 8, 2017). Are Trump and Republicans finally throwing in the towel on Obamacare? Retrieved from WashingtonPost.com on September 12, 2017.

4. Stolberg, S. (September 5, 2017). Congress Returns to a Busy Schedule. What’s on the Agenda? Retrieved from NYTimes.com on September 12, 2017.

5. Scott, D. (September 1, 2017). Senate Republicans are officially almost out of time to repeal Obamacare. Retrieved from Vox.com on September 12, 2017.

6. Everett, B. (September 7, 2017). Senate GOP accepting defeat on Obamacare repeal. Retrieved from Politico.com on September 12, 2017.

7. Kliff, S. (September 6, 2017). Cassidy-Graham: the Obamacare repeal plan McCain is supporting, explained. Retrieved from Vox.com on September 13, 2017.

8. Scott, D. (September 12, 2017). Republicans wind up one last Hail Mary to repeal Obamacare. Retrieved from Vox.com on September 13, 2017.

9. Center on Budget and Policy Priorities (July 27, 2017). Cassidy-Graham Amendment Would Cut Hundreds of Billions from Coverage Programs, Cause Millions to Lose Health Insurance. Retrieved from CBPP.org on September 13, 2017.

10. Corlette, S. and Lucia, K. (February 23, 2017). Reading The Fine Print: Do ACA Replacement Proposals Give States More Flexibility And Authority? Retrieved from HealthAffairs.org on September 13, 2017.

11. Office of Congressman Lamar Alexander (August 1, 2017). Announcing Bipartisan Health Care Hearings: Unless Congress Acts, Millions May Not Have Insurance to Buy in 2018. Retrieved from Senate.gov on September 13, 2017.

12. Office of Congresswoman Patty Murray (August 1, 2017). Senate Health Committee Chairman Lamar Alexander and Ranking Member Patty Murray Announce Health Care Committee Hearings. Retrieved from Senate.gov on September 13, 2017.

13. Kasich, J., Hickenlooper, J., et al. (August 30, 2017). Blueprint for Stronger Health Insurance Markets. Retrieved from Ohio.gov on September 13, 2017.

14. Office of Colorado Governor John Hickenlooper (September 2017). Gov. Hickenlooper’s Testimony for the Senate HELP Committee Hearing. Retrieved from Colorado.gov on September 13, 2017.

15. Stein, J. (September 12, 2017). About one-quarter of Senate Democrats now support Sanders’s single-payer health bill. Retrieved from Vox.com on September 13, 2017.

16. Cohn, J. (September 12, 2017). Ready Or Not, Here Comes Bernie Sanders And His Single-Payer Plan. Retrieved from HuffingtonPost.com on September 13, 2017.

17. Scott, D. (September 12, 2017). The most conservative Senate Democrat wants to “explore” single-payer. Retrieved from Vox.com on September 13, 2017.

18. Weigel, D. (September 12, 2017). Sanders will introduce universal health care, backed by 15 Democrats. Retrieved from WashingtonPost.com on September 13, 2017.

19. Pollack, R. (September 11, 2017). Single-payer isn’t the only progressive option on health care. Retrieved from Vox.com on September 13, 2017.

20. Stein, J. (September 8, 2017). Sen. Murphy thinks he can build an on-ramp to single-payer health care. Retrieved from Vox.com on September 13, 2017.

21. Sanger-Katz, M. (September 11, 2017). How Single-Payer Health Care Could Trip Up Democrats. Retrieved from NYTimes.com on September 13, 2017.

22. Nather, D. (September 1, 2017). Lessons for the next act on health care. Retrieved from Axios.com on September 13, 2017.

2 Likes

Senators Burr and Warner gave a press conference update on the committee’s Russia investigation on 10/4. The committee’s “goal” is crystallize their findings prior to the 2018 elections, as Russia’s active measures are still in play today & likely to ramp up ahead of the 2018 elections. The committee’s findings will hopefully provide a “road map” that other congressional committees and states can to use help protect future elections.

Things that were confirmed at the press conference: collusion is still an open question; committee (finally) endorsed the conclusions of intelligence agencies findings; Comey’s firing is not a central question, as it falls under the Judiciary Committee; claimed to “hit a wall” with verifying the explosive dossier citing Christopher Steele’s lack of response to be interviewed this claim been proven inaccurate and the committee has been in talks to interview Steele but inferred that the offers were not “credible” by publishing a statement after it was reported, by stating “we remain open to any credible offer to meet with Mr. Steele”; committee will not publicly release the Russian bought Facebook ads, but Burr stated “if any of the social media companies would like to do that, we’re fine with it” (but Facebook said that it’s up to Congress  ).

).

Coming Soon: The committee will be interviewing in open hearing: Michael Cohen on Wed, 10/25 and Facebook, Twitter & Google on Wed, 11/1.

Sources: WTFJT - Day 258, Politico, NBC

Good suggestions. I’ll add them. Want to write up a blurb for the pipeline projects?