The Paycheck Protection Program was launched to rescue the little guy, the millions of small businesses without the deep pockets needed to survive the COVID-19 shock.

But among the restaurants, dentists and mom-and-pops was Vibra Healthcare, a chain of hospitals and therapy centers spread across 19 states with over 9,000 employees. The biggest PPP loan was supposed to be $10 million, but Vibra found a way to land as much as $97 million.

In other contexts, Vibra boasts annual revenues of $1 billion, but when the company got in line to receive what is essentially free government money (the loans are forgivable), it made itself seem small. From Vibra’s corporate address in Pennsylvania, 26 limited liability companies received PPP loans, 23 of them from the same bank, with almost all the loan approvals coming on the same day in April.

ProPublica found several other large businesses employing the same apparent strategy of counting each of their LLCs or other entities as a separate business. In Las Vegas, a casino operator backed by hedge funds got 20 loans. Two nursing home chains received tens of millions of dollars: One chain in Illinois got loans for 51 different entities, while another based in Georgia got 19. Together, ProPublica was able to identify up to $516 million that flowed to just 15 organizations.

ProPublica’s findings bring into sharper focus how companies with thousands of employees were able to get assistance, just as some small businesses were reluctant to even apply. So far, the PPP has paid out more than $517 billion to 4.9 million companies — loans that can be forgiven if used to cover payroll, rent, mortgage interest or utilities. It was among the most generous of programs for businesses in the CARES Act. Loan programs for medium and large businesses spelled out in the bill generally were not forgivable. Appraisals of the PPP by economists and policymakers have been mixed: While the program did inject hundreds of billions into the economy, it did not do so efficiently, often sending aid where it was less needed, and going through banks meant well-connected businesses had a far easier time getting their share.

Amanda Fischer, policy director of the Washington Center for Equitable Growth, said there should have been enough money available to help every company quickly — even those with large payrolls. “But if we’re not going to do that, I do understand concerns about businesses that don’t technically comply, and it’s not a good look.”

“It’s Congress’ fault,” she said. “We should have helped everyone, or targeted the neediest businesses instead.”

The Small Business Administration generally defines small businesses as those with 500 employees or fewer. Congress carved an exception into the CARES Act for restaurants and hotels, allowing them to count each location as its own business, but after large restaurant chains like Shake Shack disclosed they’d taken PPP loans, the Treasury Department responded to the uproar by changing the rules to set $20 million as the maximum any one corporate group could accept. Businesses that had taken more, the government said, had to give the money back.

The chains we identified were not restaurants or hotels, but experts told ProPublica that, without knowing all the details of an entity’s control, it is difficult to say definitively whether a company had broken the program’s rules.

Fifty-one separate limited liability companies or other business entities tie back to the headquarters of Peoria, Illinois-based Petersen Health Care, which runs nursing homes and other health facilities in the region. The loans would secure at least 6,200 jobs, records show, which would total more than $52 million if the chain got the maximum amount of funding. (When the SBA released information about PPP recipients last week, it only provided ranges for the amount of each loan.)

At least 30 of those entities are nursing homes or care facilities in Illinois, according to state business documents and data from the federal Centers for Medicare and Medicaid Services. More than a third were given Medicare’s lowest 1-star rating, which the government considers “much below average” when examining health inspections, staffing and other quality measures. The loans would support about 1,900 jobs among those facilities.

The firm and its owner, Mark Petersen, did not respond to phone messages and emails seeking comment. A person who answered Petersen’s main number last week transferred ProPublica to the company’s legal department, which did not return a voicemail seeking comment.

In Maryland, a different set of 19 loan recipients traced back to an office park about 30 minutes north of Baltimore. Business records show most of those companies had another Georgia address, the home of Mariner Health Care Inc.

Mariner, which was acquired in 2004 by National Senior Care Inc. for $615 million, has 20 nursing homes and care centers in Southern California and the San Francisco Bay Area, according to its website. Those companies could receive as much as $31 million in maximum SBA funding, data shows, which could help safeguard more than 1,600 jobs.

Mariner did not answer phone calls at its main number, nor did the company respond to emails sent to an address on its website.

Another big beneficiary of the small-business program was Las Vegas-based Maverick Gaming, which has been on a casino-buying spree, backed by hedge funds, since it launched in 2017. The company owns and operates 26 casinos across three states. The company was valued at about $1 billion, Maverick CEO and owner Eric Persson told the trade magazine Global Gaming Business last year.

SBA data shows upward of $46 million going to Maverick’s companies, all of the loans arranged by the same bank. Persson, reached by phone, declined to comment.

Vibra, from its base in Mechanicsburg, Pennsylvania, specializes in hospitals that provide “post-acute” care to recovering patients. Its CEO, Brad Hollinger, has drawn on Vibra’s success to become a player on the international racing circuit: He’s a major shareholder of the British Formula One team Williams Racing. Although a car racing enthusiast, he said in 2015 that he’d bought into the team primarily for business reasons. “I am never in business not to make money,” he told Reuters.

The PPP loans are just one way the company has been buoyed by the CARES Act: Vibra hospitals have also received at least $13 million in grants for health care providers and $41 million in loans (in the form of advanced Medicare payments), according to Good Jobs First, a government and corporate watchdog based in Washington.

In publicity materials, Vibra refers to its hospitals and rehab centers as “affiliates,” but for purposes of the PPP, it appears to have treated all these LLCs as unrelated companies, receiving between $42 million and $97 million in total. Together, the companies reported retaining a total of 4,600 jobs.

Twice in recent years, Vibra has been penalized for bilking the government. In 2016, Vibra paid $33 million to the Justice Department to settle allegations that it had defrauded Medicare by admitting and keeping patients for unnecessarily long stays in order to drive up billings. Last November, Vibra paid $6 million more in a different settlement with the government; this time, it had allegedly billed Medicare for doctor visits that did not happen. In the settlements, Vibra did not admit to any wrongdoing.

There are signs that Vibra is weathering the COVID-19 outbreak well. Last month, the company announced it would manage a new hospital being constructed in Bakersfield, California. The company did not respond to multiple requests for comment.

Generally, the SBA looks at “the entirety of the organization” in determining whether businesses should be considered affiliates or separate businesses, which means taking into account “common ownership, intertwined management and economic dependence between entities,” said Megan Jeschke, a partner at the law firm Holland & Knight. In her experience defending companies accused of violating the affiliation rules, the SBA has tended to be “rigid” in interpreting the rules and frequently finds that apparently related companies are in fact affiliates, she said.

After large businesses were revealed to have taken PPP money, Treasury Secretary Steven Mnuchin said in late April that the SBA would conduct a “full review” of each PPP loan of $2 million and up. As of last week, about 29,000 such loans had been made. Given that volume, it’s unclear just how thorough the reviews might be. The SBA did not respond to a request from ProPublica seeking comment.

Last week, following pressure from watchdog groups and Congress, the Trump administration disclosed only those entities that were approved by banks for loans over $150,000. A consortium of news organizations, including ProPublica, had sued the administration under the Freedom of Information Act to release the full list of recipients and loan details.

“The vast number of PPP grants went to truly small businesses — but a lot of the money went to big businesses,” said Aaron Klein, policy director of the Brookings Institution’s Center on Regulation and Markets. “The media attention is going to focus, and crystallize, how much big businesses got out of this program.”

Did Your Company Get Bailout Money? Are the Employees Benefiting From It?

ProPublica is reporting on the government’s various programs to support businesses amidst the epidemic. We want to know what these programs mean for your workplace. Please help us report.

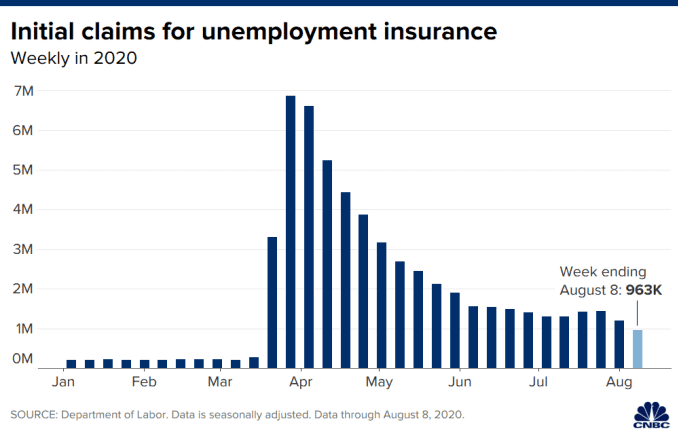

First-time claims for unemployment insurance last week fell below 1 million for the first time since March 21 in a sign that the labor market is continuing its recovery from the coronavirus pandemic.

The total claims of 963,000 for the week ended Aug. 8 were well below the estimate of 1.1 million from economists surveyed by Dow Jones. That represented a decline of 228,000 from the previous week’s total.

Jobless claims had totaled above 1 million for 20 consecutive weeks as the U.S. economy went into lockdown to contain Covid-19. The last time the total was below that number was March 14, with 282,000, just as the pandemic declaration first hit.

While the sub-1 million reading marks a milestone, there’s still plenty of work to do for the job market to get back to normal. Those collecting benefits for at least two weeks, known as continuing claims, totaled nearly 15.5 million, a decrease of 604,000 from a week ago, but still well above pre-pandemic levels.

Vox’s Emily Stewart joins Dara and Jane to discuss the relationship between “the market” and the “real economy.”

Resources:

“The Stock Market Is an Engine of Civic Destruction” by Libby Watson, New Republic

“Who gets to be reckless on Wall Street?” by Emily Stewart, VoxHosts:

Dara Lind (@DLind), Immigration reporter, ProPublica

Jane Coaston (@cjane87), Senior politics correspondent, Vox

Emily Stewart (@EmilyStewartM), Reporter, Vox

The S&P 500 closed at a record on Tuesday, a remarkable display of investor optimism in the face of a still-shambolic American economy.

But aside from standing as testament to the sunny disposition of stock market investors, the record high also confirms the transfer of power from Wall Street’s pessimists — or “bears” — to the “bulls” who see more gains ahead.

Simply put, the record on Tuesday confirms that American investors are in a bull market again. We say ‘confirmed’ because the start of the bull market is actually traced back to when stocks hit rock bottom — which means it has been going on since March.

There’s no science behind the system for determining the start or end of a bull or bear market. It’s just tradition.

By that tradition, entry into a bear market is confirmed once stocks have fallen 20 percent from their high. That happened in mid-March, after the market crashed as the coronavirus crisis slammed the United States.

A bull market has its own criteria. Even though stocks were already up more than 50 percent from their lowest point (hit on March 23), some market traditionalists say that the bull market is only confirmed once stocks close at a record. That’s what just happened.

Why does any of this matter? Because markets often operate as something of an experiment in mass psychology. There’s a symbolic value to whether commentators, the news media and even the president are able to describe the context of the market as good or bad.

The last bull market grew out of the ashes of the 2008 financial crisis, with the S&P 500 beginning its run in March 2009, and rising more than 300 percent in almost 11 years.

That doesn’t mean the current bull market will last as long. The last one was about twice as long as usual. But this one is just getting started.

The U.S. economy shrank at an alarming annual rate of 31.7% during the April-June quarter as it struggled under the weight of the viral pandemic, the government estimated Thursday. It was the sharpest quarterly drop on record.

The Commerce Department downgraded its earlier estimate of the U.S. gross domestic product last quarter, finding that the devastation was slightly less than the 32.9% annualized contraction it had estimated at the end of July. The previous worst quarterly drop since record-keeping began in 1947 was a 10% annualized loss in 1958.

Last quarter, businesses shuttered and millions of workers lost jobs as the world’s largest economy went into lockdown mode in what succeeded only fitfully in limiting the spread of reported viral infections. The U.S. economy fell an annualized 5% in the first three months of the year as the coronavirus began to make its presence felt in February and March.

A bounce-back in hiring as many businesses reopened suggested that the economy began to recover in June with third quarter growth estimated to be around 20% annualized. But economists say a full recovery remains far off given that the virus has yet to be contained and the government’s financial support has faded.

“As we approach the fall, we see four important risks for the economy: a failure to provide further fiscal stimulus, a second wave of COVID-19 infection during the flu season, major election uncertainty and rising trade tensions with China,” said Lydia Boussour, senior U.S. economist at Oxford Economics.

Unemployment is still high at 10.2%, and roughly 1 million people are applying for jobless aid each week even as the amount of aid they receive has shrunk. Consumer confidence has tumbled. Though the stock market and home sales are surging, the broader economy shows signs of stalling, and millions face potential evictions from their homes.

The challenges reflect the unusual nature of the downturn. Many U.S. households have increased their savings and paid off debt—which could either signal a hesitancy to spend as they have in the past or pent-up demand that could be unleashed once the pandemic ends.

Just over 1 million Americans applied for unemployment benefits last week, a sign that the coronavirus outbreak continues to threaten jobs even as the housing market, auto sales and other segments of the economy rebound from a springtime collapse.

The Labor Department reported Thursday that the number of people seeking jobless aid last week dropped by 98,000 from 1.1 million the week before.

The number of initial claims has exceeded 1 million every week but one since late March, an unprecedented streak. Before the coronavirus pandemic, they had never topped 700,000 in a week.

“Layoffs are ongoing reflecting interruptions to activity from virus containment that are likely resulting in permanent closures and job losses,” Rubeela Farooqi, chief U.S. economist at High Frequency Economics, wrote in a research report.

Farooqi added that “the risk of permanent damage to the labor market remains high which will slow the pace of recovery. The return to pre-pandemic levels of prosperity is set to be an uncertain and prolonged process.”

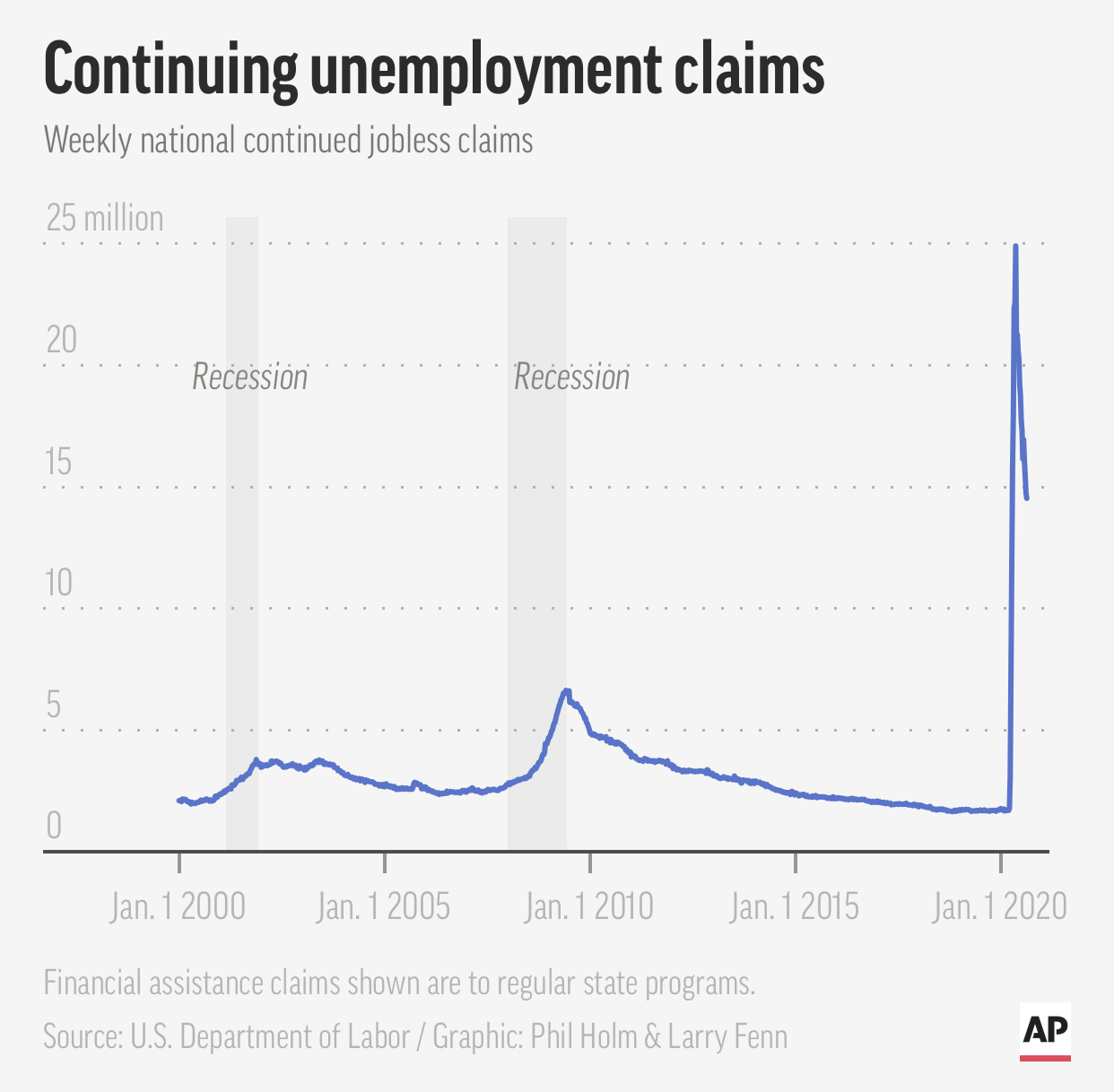

More than 14.5 million are collecting traditional jobless benefits – up from 1.7 million a year ago – a sign that many American families are depending on unemployment checks to keep them afloat.

U.S. debt has reached its highest level compared to the size of the economy since World War II and is projected to exceed it next year, the result of a giant fiscal response to the coronavirus pandemic.

The Congressional Budget Office said Wednesday that federal debt held by the public is projected to reach or exceed 100% of U.S. gross domestic product, the broadest measure of U.S. economic output, in the fiscal year that begins on Oct. 1. That would put the U.S. in the company of a handful of nations with debt loads that exceed their economies, including Japan, Italy and Greece.

This year the ratio is expected to be 98%, also the highest since World War II.

Dang, that’s bad. I mean if you’re the kind of person who stresses out about the US debt to GDP ratio. This was a thing people used to argue about right?

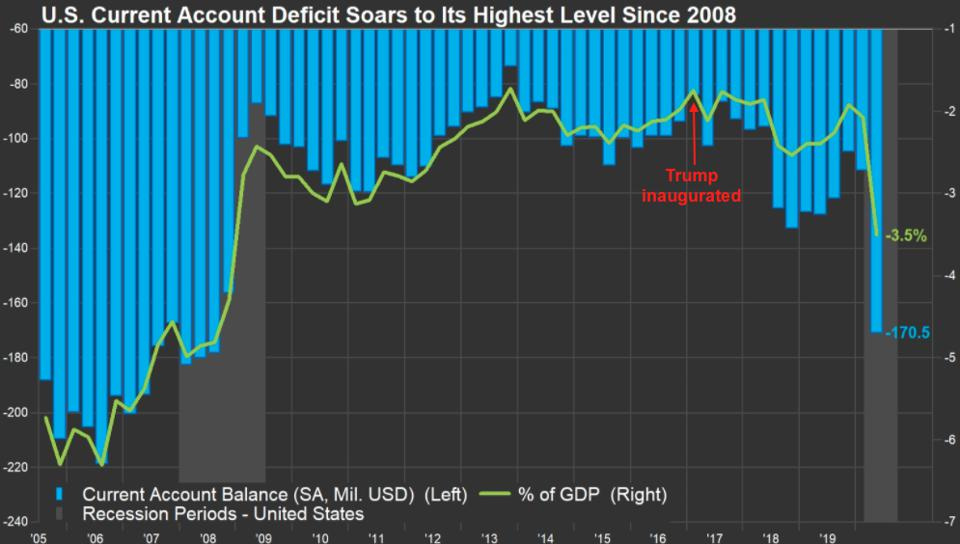

The U.S. trade deficit jumped 18.9% in July owing to a big snapback in imports, the government said Thursday. The trade gap increased to $63.6 billion from $53.5 billion in the prior month - above the $58.9 billion MarketWatch forecast. Imports shot up 10.9% while exports advanced 8.1%. The increase in both imports and exports is a good sign in many ways, pointing to stronger consumer spending at home and increased demand for American-made goods abroad. Yet global trade is still considerably weaker compared to before the coronavirus pandemic and it will take time to recover. U.S. exports, for example, were 26% lower in July compared to the same month in 2019.

Another 881,000 people applied for state unemployment benefits last week, the Labor Department says. That’s 130,000 fewer than the previous week. But the report comes with an asterisk.

The department just changed the way it adjusts claims data to account for seasonal variation. That should make the reports more accurate in the weeks to come. But it also means the reported change from the previous week is not an apples-to-apples comparison.

Without the seasonal adjustment, state unemployment claims rose by more than 7,500.

In addition to the state unemployment claims, 759,000 people applied for benefits under a special federal program for gig workers and the self-employed, who are ordinarily not eligible for unemployment. Those claims also increased from the previous week.

I missed this when it came out four months ago. Oh no, 267 billionaires stopped being billionaires! Poor things!

Donald Trump lost an estimated $1bn of his paper fortune in the past month as the coronavirus lockdown forced the closure of offices, shopping centres, hotels and golf courses he owns.

The US president’s fortune has fallen from an estimated $3.1bn (£2.5bn) on 1 March to $2.1bn on 18 March (at the height of stock market panic caused by the coronavirus pandemic) according to Forbes magazine’s annual billionaires list.

The Covid-19 induced collapse in global stock markets led to 267 of the world’s richest people losing their billionaire status, in the magazine’s 34th annual wealth ranking. There are now 2,095 dollar billionaires in the world – and a record 1,062 of them have lost money compared with last year.

Among those who joined the billionaires’ club is Eric Yuan, the founder of Silicon Valley video conferencing app Zoom. The magazine estimates that Yuan, who owns 20% of Zoom’s shares, has a paper fortune of $5.5bn.

The app has become hugely popular during the coronavirus lockdown as people around the world use it to keep in touch. Zoom has been used for everything from nursery school sing-alongs to FTSE 100 boardroom meertings and even UK Cabinet meetings.

But Yuan was forced to apologise to users over misleading claims that it offers “end-to-end encryption for all meetings”. “We recognise that we have fallen short of the community’s – and our own – privacy and security expectations,” Yuan said in a blog post. “For that, I am deeply sorry.”

Amazon founder and chief executive, Jeff Bezos, maintained his standing as the world’s richest person for the third consecutive year with a $113bn fortune. His total wealth estimated by Forbes slipped from $131bn last year. Amazon’s shares have largely recovered from the stock market plunge as most of the company’s services are still operating throughout the lockdown.

Most of Trump’s wealth comes from his real estate. His Trump Organization empire – which is managed by his sons Donald Jr and Eric – includes Trump Tower in Manhattan and his Mar-a-Lago club in Florida, which the president likes to call his “winter White House”). There are also more than a dozen hotels and golf courses, such as the Trump International Hotel above the Las Vegas strip and the Trump International Golf Links in Aberdeenshire, Scotland.

World governments and many US states have forced the closure of all non-essential businesses across the world, leaving offices and hotels empty and golf courses deserted.

The Trump Organization has closed 17 of its properties across the world, according to the Washington Post. Those that are still open are running skeleton services. About 1,500 Trump Organization staff have been laid off or furloughed, according to public filings reviewed by the newspaper.

The closed properties generated about $650,000-a-day for the company, according to the president’s previous financial disclosures.

The Trump Organization last week sought guidance from Florida’s Palm Beach county about whether it expected the company to continue making monthly payments on land it leases for a 27-hole golf club, the New York Times reported. Trump representatives have also reached out to Deutsche Bank, the company’s largest creditor, about the possibility of postponing payments on some of its loans.

Forbes said it calculated Trump’s fortune by comparing it to the share price plunges experienced by stock market-listed real estate companies, which suffered average stock price declines of 37%. The magazine also compared Trump’s hotel and golf businesses with listed hospitality companies, which have also suffered heavily in the stock market rout.

Trump also owns 125,000 sq ft of retail space near Fifth Avenue in Manhattan. It is normally one of the most profitable shopping areas in the world, but has been deserted for weeks due to the pandemic.

Eric Anton, a New York property broker, said: “The [Forbes] analysis, it’s as good as any other way I can think of [estimating Trump’s wealth].”

• This article was amended on 17 April 2020 to describe the location of the Trump International Hotel as “above the Las Vegas strip” rather than on the strip.

About that tax cut…

The Dow Jones Industrial Average dropped more than 800 points Monday following a report that large global banks were involved in transactions flagged as possible money laundering.

And hopes for another stimulus measure from Congress flagged as lawmakers focused on a fight over a Supreme Court nomination following the death of Justice Ruth Bader Ginsburg.

The Dow dove 3% and the broader S&P 500 index fell 2.5% in afternoon trading. The Nasdaq composite index was down 1.6%.

Bank stocks fell after a news report that JPMorgan Chase, Deutsche Bank and other giant banks defied money-laundering crackdowns. JPMorgan Chase fell more than 4%, Citigroup was down 3% and HSBC was down 6%.

A surge in COVID-19 cases in the United Kingdom raised fears of another lockdown there. Lockdowns have ripple effects that hurt several industries, including travel. Airlines stocks plummeted Monday, with United Airlines down 7.5% and American Airlines down 6.4%.

Stocks have had a rough September. The Dow has fallen more than 5% so far this month.

Another factor weighed on the market on Monday. Over the weekend, China announced rules for a new regulatory body that could blacklist foreign companies that unfairly treat Chinese companies or pose a threat to Chinese national security, NPR’s Emily Feng reported.

China has not yet said which companies would be labeled “unreliable entities” but Chinese state media have suggested that U.S. tech companies including Apple, Qualcomm and Cisco would be considered. U.S. tech stocks, which led the market to new records, have been sliding in recent weeks.

The latest tensions with China come as the Trump administration has threatened to bar the Chinese-owned TikTok and WeChat apps in the U.S.

The U.S. economic slowdown amid the coronavirus pandemic also continues to worry investors. Retail sales grew more slowly in August after an extra $600 per week in federal unemployment benefits expired.

The Federal Reserve has cut interest rates to historic lows and says it expects to keep them down through at least 2023, but Congress has been deadlocked about providing additional pandemic economic assistance. The debate over whether President Trump should be allowed to name a successor to Ginsburg could dampen hopes for a stimulus deal.

Cross posting, forgot Econ news usual comes out Thursdays, it is Thursday isn’t it?

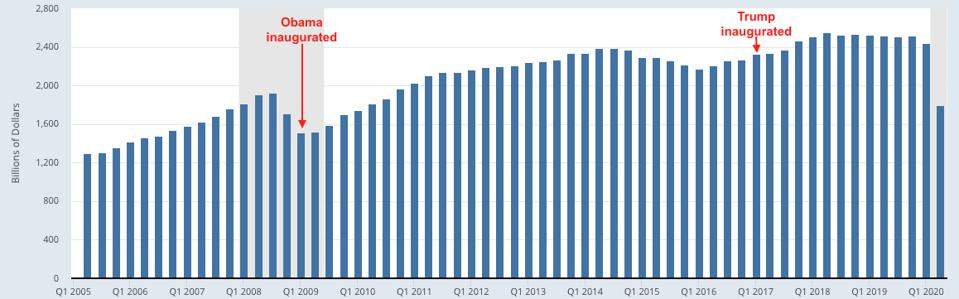

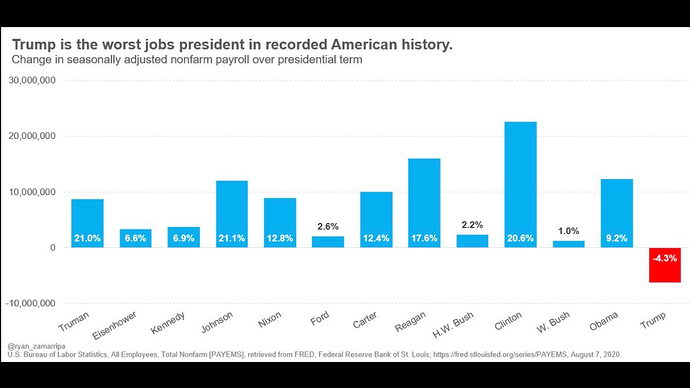

President Trump campaigned on reducing if not eliminating the U.S. trade deficit. He has failed to deliver on this as the trade deficits in 2018, 2019 and based on the current pace for 2020 they will be the largest since 2008, before President Obama took office.

While Trump talks about trade deficits, what he has really focused on is the Goods deficits as Services from the U.S. runs a surplus. The graph below shows how the gap in Goods exports and imports has remained fairly stable and has actually grown over the past two years. In August 2018 the Goods deficit was approximately $70 billion and it has grown to $82.9 billion in August this year.

Sara Potter from FactSet Research Systems wrote, “Looking ahead, the monthly data we have so far for international flows in the September quarter isn’t encouraging. The U.S. Census Bureau reported earlier this month that the July trade balance of goods and services fell to negative $63.6 billion, the biggest deficit since July 2008. The services balance, where the U.S. maintains a surplus, fell to its lowest level in eight years; at the same time, the goods deficit fell to an all-time low of $80.9 billion (balance of payments basis). While both exports and imports have recovered somewhat in recent months from their recent lows, exports of goods and services remained down 20.1% in July compared to a year ago while imports were off by 11.4%.”

While trade does negatively impact sectors of the economy and the jobs associated with them, overall it tends to be a net benefit to the economy. Consumers receive lower prices and/or a wider range of goods and companies gain access to additional markets. Unfortunately, Trump’s lack of understanding of trade’s benefits has overwhelmed his desire to see it reduced, if not eliminated.

One aspect to the chart below shows how increasing exports help the economy grow. However, when Trump started various trade wars they flattened out. Exports then took a nosedive when countries around the world shut down due to the coronavirus.

China Phase One trade deal

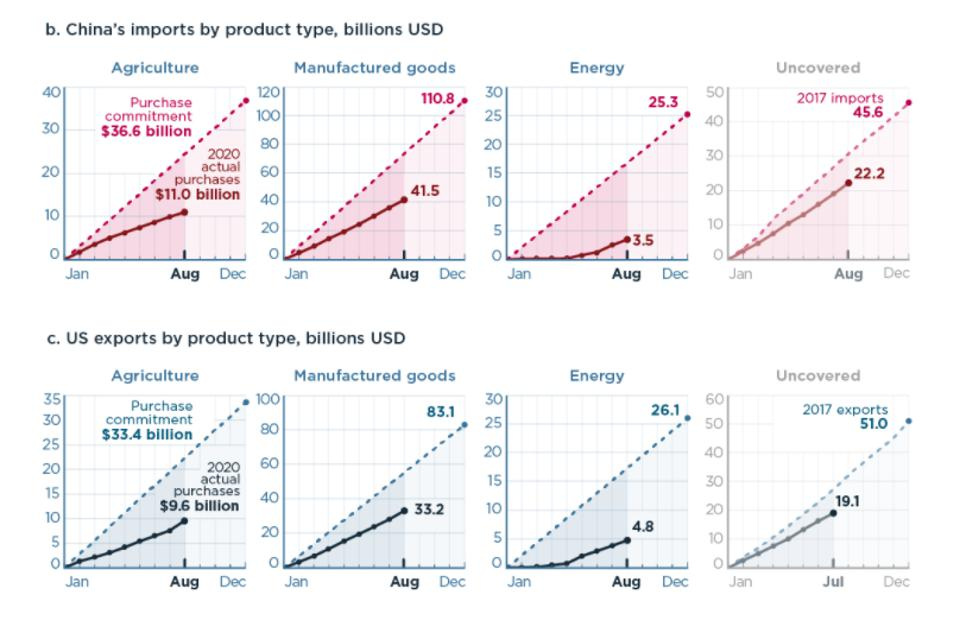

Trump’s Phase One trade deal with China is woefully behind on where it should be. While the coronavirus does have a lot to do with this, even before it hit exports to China lagged and had goals that were going to be very hard to achieve.

Chad Bown from the Peterson Institute for International Economics has been tracking the amount of U.S. exports to China and how they stack up to the Phase One trade deal. He wrote, “Through August 2020, China’s year-to-date total imports of covered products from the United States were $56.1 billion, compared with a prorated year-to-date target of $115.1 billion. Over the same period, US exports to China of covered products were $47.6 billion, compared with a year-to-date target of $95.1 billion. Through the first eight months of 2020, China’s purchases of all covered products were thus only at 50 percent (US exports) or 49 percent (Chinese imports) of their year-to-date targets.”

Note that the difference between the Chinese imports and U.S. exports numbers is due to, “As set out in the legal agreement, one 2017 baseline scenario allows for use of US export statistics and the other allows for Chinese import statistics” per Bown, which also comes into play for the full year amounts.

Bown also points out that, “prorating the 2020 year-end targets to a monthly basis is for illustrative purposes only. Nothing in the text of the agreement indicates China must meet anything other than the year-end targets.”

So far China has imported about half of their full year commitments but the year is two-thirds over.

This topic was automatically closed 15 days after the last reply. New replies are no longer allowed.